Auditing LLM Trading Bridging Theory and Market Reality with the GT table in R

News Source : R-bloggers.com

News Summary

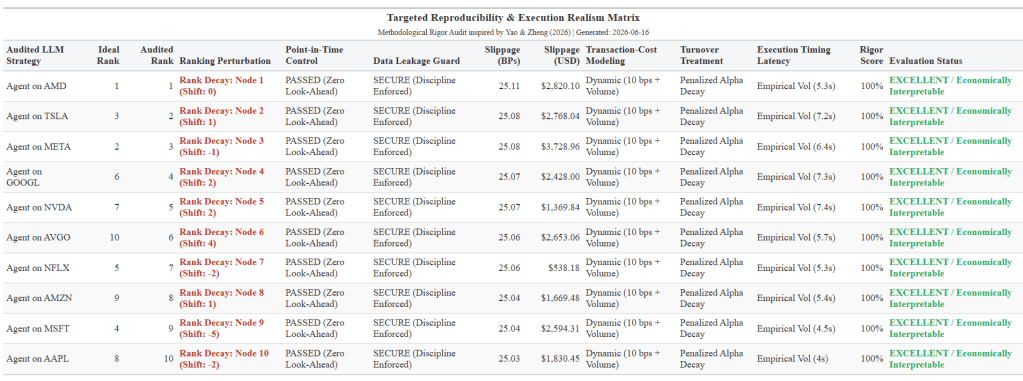

- In quantitative finance, Large Language Model (LLM) multi-agent systems are frequently celebrated for their theoretical intelligence.

- Traditional backtests systematically ignore execution semantics and market microstructure realities.

- In AI-driven trading systems, the primary risk is no longer the raw quality of the agent’s alpha signal; it is the cognitive latency required to generate that signal.

- Yao & Zheng (2026) forces us to stop judging agent architectures by their abstract zekası, and start auditing them by the brutal financial reality of their execution timing.

[This article was first published on DataGeeek, and kindly contributed to Rbloggers]. (You can report issue about the content on this page here) Want to share your content on Rbloggers?